Studies have shown that the bulk of the returns generated by investment is dictated by asset allocation. If you are looking to grow your wealth over time, fixed-income investments, like annuities, which offer fixed payments that can neither grow nor shrink, aren’t likely to get the job done. Why? Because inflation can take an enormous chunk out of your savings.

How Inflation Shrinks Savings?

Let’s say you've got ₹100 in a savings account that pays a 1% interest rate. A year later, you will have ₹101 in your account. But if the rate of inflation is running at 2%, you would need ₹102 to possess an equivalent buying power than you started with. You've gained a rupee but lost buying power. Any time your savings don’t grow at an equivalent rate as inflation, you will effectively lose money. If you are a retiree living on your savings, you can’t continue the same standard of living if inflation cuts into your purchasing power with every passing year.

This is especially true in India, where costs tend to rise at a greater rate than in many other developed countries. Inflation can hurt well before retirement. If you are steadily saving money with a goal in mind, like a college fund for your children or a down payment on a home, the purchasing power of your money may decline while you're saving it.

Inflation is a market force that is impossible to avoid entirely. But by planning for it and putting a robust investment strategy in situ, you might be able to help minimize the impact of inflation on your savings and long-term financial plans.

Thus, in today’s world, just earning money isn't enough, which is why investments are important. You would like to have your money exerting for you. This is often why you ought to invest. Money lying idle in your vault at home is a lost opportunity. You need to invest that cash smartly to urge good returns out of it. Asset-allocation strategies can help you diversify and understand how to make picking the right mix of securities the core of your investing strategy.

Purpose of Diversification

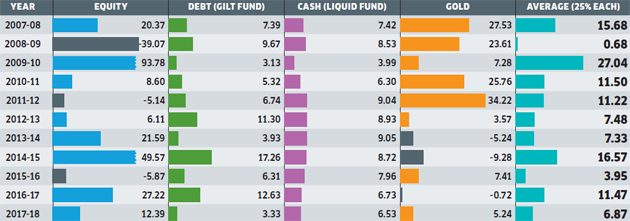

Traditional wisdom says don’t put all of your eggs in one basket. It restricts the damage to your economic well-being in case one asset class or instrument goes for a tailspin. In 2008-09, if you had spread your investments across equity, debt, cash and gold, the portfolio would have given a mean return of 0.68%. This is due to the brilliant performance of gold (up 24%) and stable returns from cash and debt during that year. The situation reversed the subsequent year, with equities rising 94% and all other asset classes giving lacklustre returns. Even so, the diversified portfolio managed to get 27% returns that year.

A Diversified Portfolio can give Decent Returns

Year-wise returns from some asset classes have been quite volatile within the 11 years since 2008-09. The diversified portfolio was more stable.

Figures are returns from the asset classes during the fiscal year. Negative returns are marked in grey.

Investing in equities entails more risk, but is also statistically likely to steer greater returns. Investors who want to avoid the volatility associated with individual stocks might choose mutual funds, which are professionally managed and aim to provide a good return over time.

Don’t Overdiversify

Some investors are under the assumption that the greater the diversification, the higher the returns and they keep adding stocks to their portfolios. Consistent with modern portfolio theory, 15-20 stocks from different sectors are enough to form a well-diversified equity portfolio of ₹50 lakhs-₹60 lakhs. This is often because diversification can reduce market risks only up to a limit. Since the risk can’t be diversified away, there is no purpose in carrying on.

Importance of Cash

However, cash deserves respect. The goal of cash isn't always to generate a return for you. The aim of savings is parking it in extremely safe and liquid (meaning they can be sold or accessed in a very short amount of time; at most, a few days) securities or accounts. This comes in handy during challenging times.

As a general rule, your savings should be sufficient to provide for all of your personal expenses, including your mortgage, loan payments, insurance costs, utility bills, food and clothing expenses for a minimum of three to six months. That way, if you lose your job, you will have sufficient time to adjust your life without the extreme pressure that comes from living paycheck to paycheck.

Any specific purpose in your life that will require an outsized amount of money in five years or less should be savings-driven, not investment-driven. The stock exchange in the short run is often extremely volatile, losing more than 50% of its value in a single year.

It’s time to be smart and to get wealth.